Aspire Review (2026)

Aspire Review (2026)

Finance tools are trust-critical: the bar is accuracy, compliance and real support, not flashy features. So where does Aspire actually fit?

Visit Aspire → Affiliate link — the rest of this page is the honest version, including who should skip it.

Watch the 2-minute review

Same honest take, in video form — from our YouTube channel.

⚡ Short on time? Watch the 30-second verdict Short.

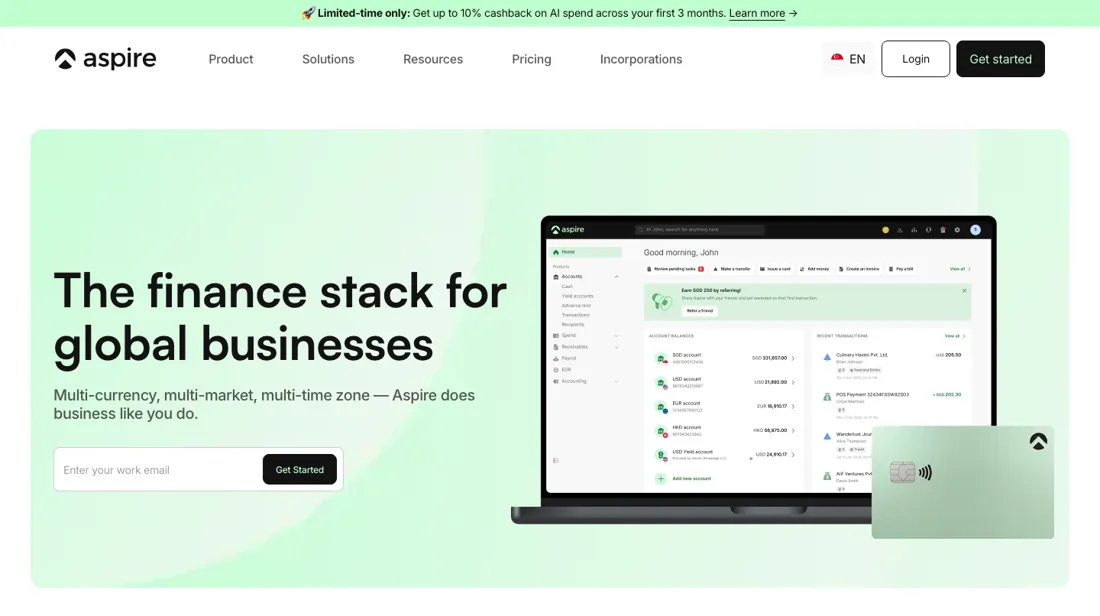

What Aspire does

All-in-one finance stack for global businesses: multi-currency accounts (30+ currencies), corporate cards with 1.2% cashback, expense management, bill pay, payments and payroll — with AI fraud detection and multi-admin approval workflows.

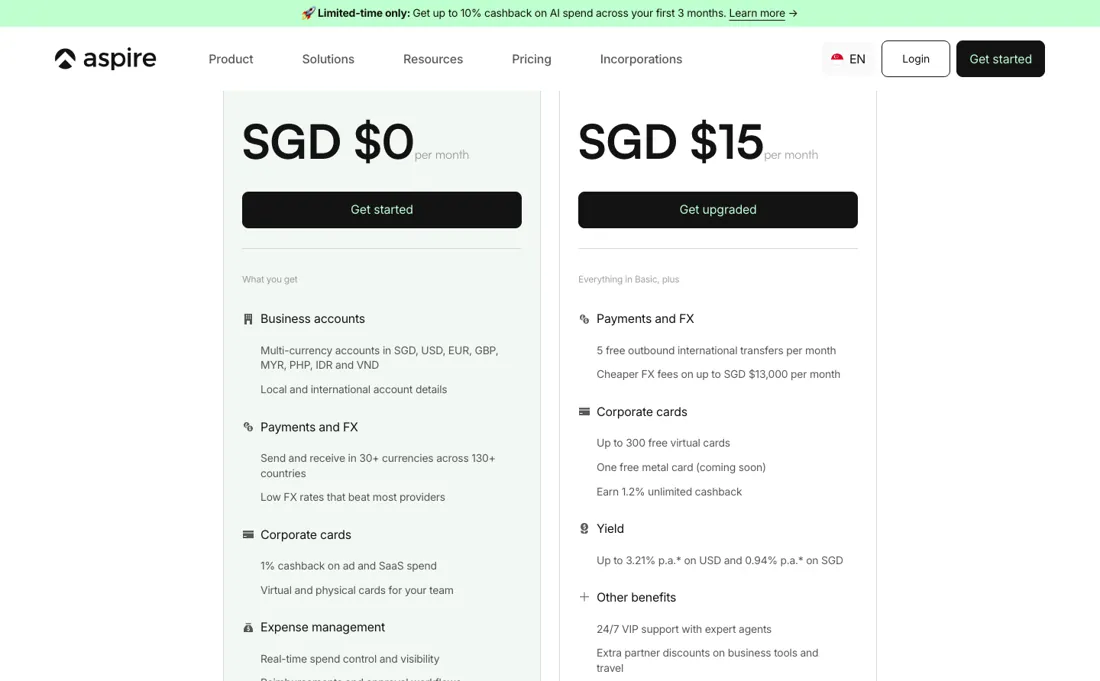

Pricing (2026)

$0 monthly fee, no minimum balance and no deposit to open; you pay per use — FX conversion markups on international transfers and a per-transfer fee on outbound SWIFT — with a paid Premium tier for heavy international senders (2026). Plans change — always verify the live price on their site.

What the pricing page doesn’t say

It's a fintech account (strongest in Southeast Asia), not a full bank — great for keeping fixed costs near zero on mostly-domestic activity, but confirm it supports your country and currencies before you build your finances around it.

What buyers report about Aspire

Recurring themes from Trustpilot, Statrys and Reddit, read in August 2026. We have not run Aspire ourselves, so this is other buyers' experience rather than ours. We summarise it here because the complaints are usually the part a vendor page leaves out.

- • Onboarding with no paperwork is the recurring praise, particularly from first-time founders comparing it to a traditional bank.

- • For mostly domestic SGD activity the S$0 monthly fee and free local transfers do what they claim.

- • Sudden account closures and holds on funds, with little explanation, surface repeatedly across Trustpilot and Reddit. Compliance reviews triggered by regular payments to accounting and advisory firms are a specific recurring pattern. If your outgoings look like that, plan a fallback account.

- • Promotions carry terms in the fine print that reviewers say they did not expect.

- • Support experience is genuinely inconsistent — the same platform gets called both prompt and terrible in the same month.

When the paid plan is worth it

Aspire's Basic plan is SGD $0/month; Premium is SGD $15/month (Singapore/SGD pricing). Premium pays back if you send international transfers or convert FX regularly. It waives up to 5 outbound SWIFT transfers per month (the vendor values this at up to USD $75/month) and gives mid-market FX on your first SGD $13,000/month of conversions, versus Basic's "from 0.23%" send / "from 0.34%" receive. It also lifts free spend users from 5 to 10 and cashback from 1% (ads/SaaS only) to 1.2% on all eligible spend, and halves the yield-account fee from 0.5% to 0.25%. What upgrading does NOT fix: the 0% FX window is capped at SGD $13,000/month, then you pay from 0.22%; inbound SWIFT fees (SGD $35 / USD $8) still apply; and it adds no banking licence, lending, or extra country coverage. If your activity is mostly domestic and low-volume, Basic already costs nothing and Premium is dead weight.

How to actually use Aspire

You sign up with a work email, verify by OTP, then pick your country of incorporation, industry, entity type and source of funds. You upload company documents through the app or web dashboard: an ACRA business profile for Singapore companies (Certificate of Incorporation plus Business Registration Certificate for Hong Kong ones), director ID or passport, proof of address, and a director facial verification. First login runs on OTP codes sent to both your email and phone, plus the ID number and birth date from registration. The vendor advertises approval "as fast as 1 day," but a hands-on independent review reports 1–5 business days is more typical, stretching to 5–15 if a compliance review is triggered. Where people actually stall: document re-requests over mismatched names or expired certificates, an industry getting flagged higher-risk, unclear source-of-funds answers, and — per that same review — some accounts being paused months in with limited explanation. Answer document requests fast; slow replies extend the timeline. Distilled from vendor docs (help.aspireapp.com first-login guide) and one hands-on independent review (growacross.com), which discloses several months of first-hand onboarding and usage.

The natural comparison is Wise Business or a local business bank — other multi-currency fintech accounts. Decide by which one fits the job above, not by the louder brand.

See the full Aspire vs Wise Business head-to-head →

More on Aspire

Everything we publish about Aspire links back here — the review stays the honest hub:

My ex-banker filter is simple: does Aspire remove a real cost — time, errors, missed revenue — bigger than what it charges? If the job above is genuinely yours, it's worth a look. We never publish fake or “exclusive” prices, so always confirm the current plan on their site.

Frequently asked questions

Is Aspire safe to run my finances through?

The bar here is higher than features. Check who actually holds the money and under what licence, whether client funds are segregated, what audit trail and permission controls you get, and how support behaves when something goes wrong mid-transaction. Anything touching payments should be able to answer those in writing; if it cannot, that is your answer.

Who should not use Aspire?

Skip it if you need a traditional bank relationship, lending, or coverage in a region Aspire doesn't serve — check availability first. Buying a tool to fix a problem you don't have yet just adds cost and another login to manage.

Is this a hands-on review of Aspire?

This is a researched assessment, not a hands-on test — where we've used a tool ourselves, we say so explicitly. We name what each tool is genuinely good and bad at, and we earn a commission only if you sign up, at no cost to you.

- Buyer reviews on Trustpilot, Statrys and Reddit, read August 2026.

- Aspire’s own published pricing page.

- A dated screenshot of that pricing page, kept on this site as the receipt.

We list our sources because most review sites do not. How we review →

Others in this category

Weighing Aspire against the field? These are the financial operations tools closest to it that we have also reviewed. They overlap rather than match, so check what each one is actually built for before treating any of them as a swap:

New dossiers, cost-traps we found, and tools that earned a keep — no hype, no sponsored-disguised-as-advice. Unsubscribe anytime.

This is our researched assessment — not a paid placement. The “Visit” links on this page are affiliate links: we may earn a commission if you sign up, at no extra cost to you, and it never changes our take. How we review →

Spotted an error? Tell us — we verify and fix fast, whether or not it flatters the product.